|

|

Federal Reserve Likely To Dial Back Rate Hikes But They’re Far From Over

|

|

The Federal Reserve System’s aggressive rate-hike campaign of 2022 is likely to be dialed back when U.S. central bankers meet in two weeks but is far from over.

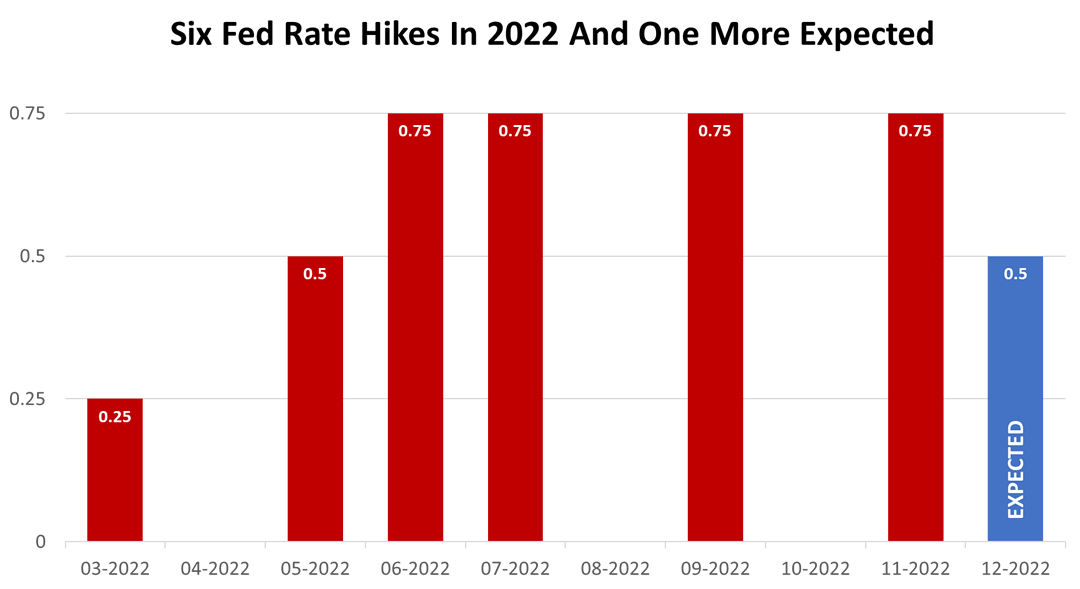

Federal Reserve Chair Jerome Powell, in a speech today at the Brookings Institution, said a 50-basis-point rate hike would be on the table at the Fed’s December 13 and 14 policy meeting. Since March, the nation’s central bank has raised lending rates six times. After a quarter-point hike in March and a half-point hike in May, the Fed hiked rates four more times by three-quarters of 1% in an aggressive effort to end inflation by slowing economic growth. Fed chair Powell’s remarks offered no big surprises but did go into more detail than previous public pronouncements about how a shortage of workers is making inflation harder to control. Here’s a summary of important points investors need to understand: - Inflation remains near a 40-year high and has only begun to show signs of slowing from its current level, and the Fed’s preferred metric of inflation – the Personal Consumption Expenditure Deflator index – must drop from its current level of about 6% much closer to the Fed’s target rate of 2% to prompt a reversal in monetary policy.

- The rate hike cycle has slowed growth in economic activity to well below its longer-run trend rate of about 2% but this trend must be sustained by the Fed.

- Supply chain bottlenecks in goods production are easing and goods price inflation appears to be easing as well, and this, too, must continue.

- Housing services inflation, which measures the rise in the price of all rents and the rise in the rental-equivalent cost of owner-occupied housing, has continued to rise sharply and will probably keep rising well into next year, but we will likely see housing services inflation begin to fall later next year.

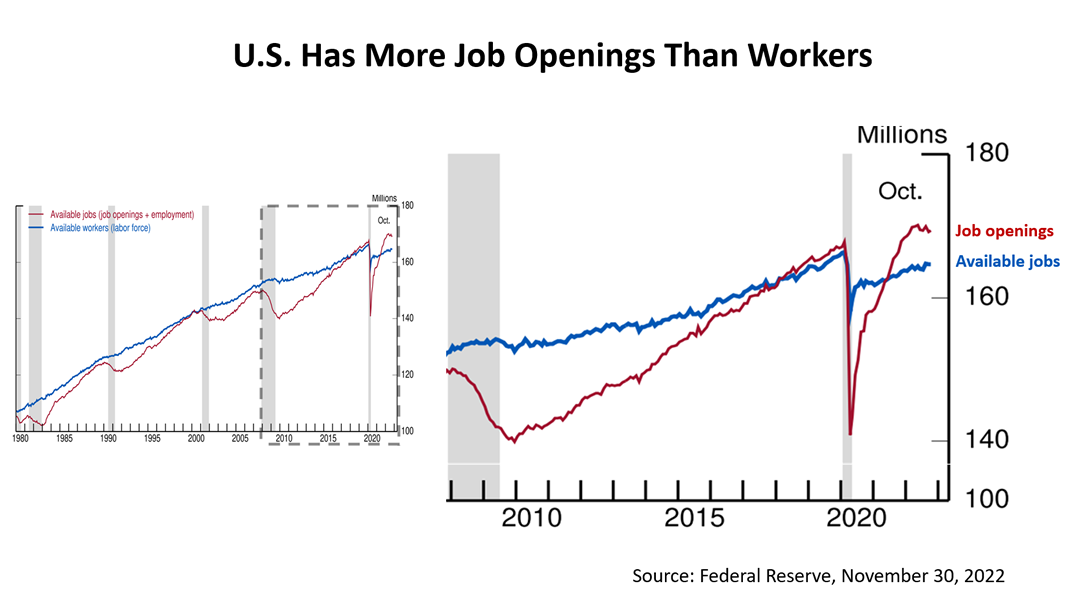

- A very important factor in inflation in 2023 will be the labor market, which is out of balance. The U.S. has a shortfall of about 3.5 million workers. The illustration above shows the shortfall on the right and shows that this imbalance has not occurred in over 40 years. Wage growth remains well above levels that would be consistent with 2% inflation over time.

- The labor shortage reflects both lower-than-expected population growth and a lower labor force participation rate. Participation in the labor force by those from age 16 to 65, dropped sharply at the onset of the pandemic because of sickness, caregiving, and fear of infection. It was expected that participation in the labor force would return as the pandemic faded. For workers in their prime working years, it mostly has. Overall participation, however, remains well below pre-pandemic trends.

- Part of the shortage reflects workers who left the labor force because they are sick with COVID-19 or continue to suffer lingering symptoms from "long COVID". But recent research by Fed economists finds that the participation gap is now mostly due to excess retirements — that is, retirements in excess of what would have been expected from population aging alone. These excess retirements might now account for most of the shortfall in the labor force.

“Price stability is the responsibility of the Federal Reserve and serves as the bedrock of our economy,” Mr. Powell said. “Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all.”It is likely that restoring price stability will require holding policy at a restrictive level for some time. History cautions strongly against prematurely loosening policy,” Mr. Powell said. “We will stay the course until the job is done.” Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. You should consult the appropriate financial professional regarding your specific circumstances.

The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions.

This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice. |

|

|

| This article was written by a professional financial journalist for Responsive Financial Group, Inc and is not intended as legal or investment advice. |

|

| ©2024 Advisor Products Inc. All Rights Reserved. |

|

|

|

|

|