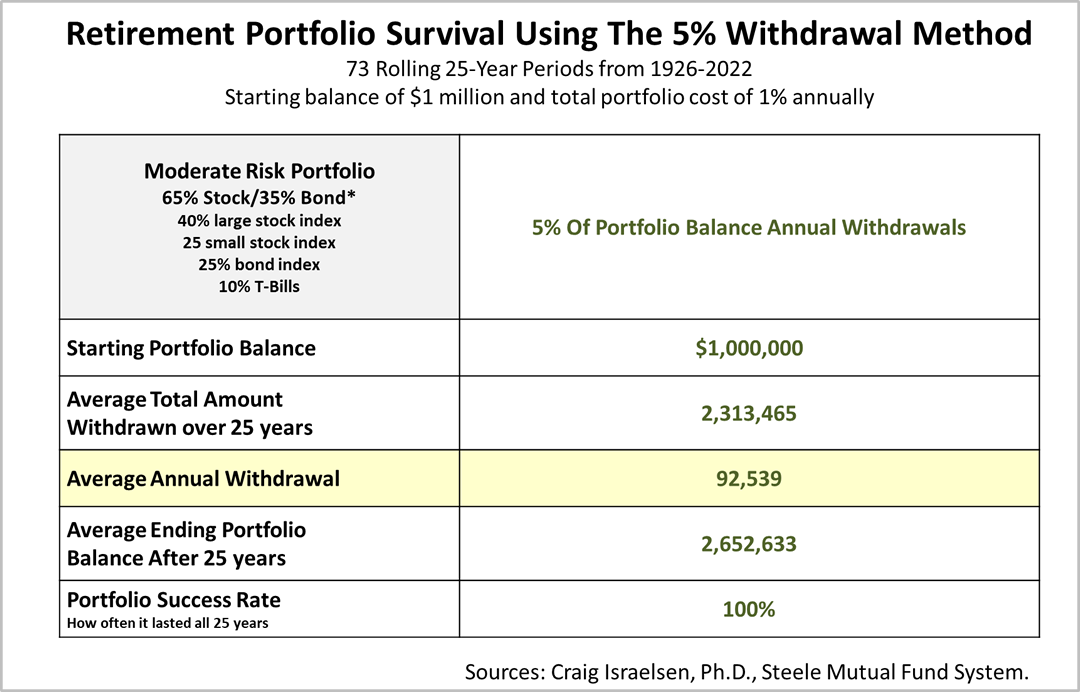

One of the most important concepts for a pre-retiree or retiree to understand is the difference between withdrawing a set amount of money each year versus withdrawing a percentage of a portfolio’s year-end balance. Are you going to be annually pulling out a prescribed amount from your retirement portfolio — $50,000 or $60,000, or whatever? Or are you pulling out a percentage -- four, five, six percent or more – every year. The difference between these two withdrawal approaches can make a very big difference in your retirement security and in how much you leave your children, other loved ones, and charity. Choosing the best withdrawal method in your personal situation often depends on whether you want to extract as much income as possible in retirement or prefer to leave as much as possible to your spouse and other loved ones. This article illustrates this key concept in retirement planning in real-life detail. The calculations and withdrawal methods in this analysis are from Craig Israelsen, a college professor of family financial management for over three decades and leading educator on low-expense investment planning, who is currently Executive-in-Residence in the Financial Planning Program at Utah Valley University. Assumptions. To illustrate the concept, we’re assuming the withdrawal phase of the portfolio extends 25 years, providing annual withdrawals to a retiree until age 90. The portfolio was diversified by investing 40% in large-company stocks, 25% in small company stocks, 25% in 10-year U.S. Treasury bonds, and 25% in 90-day U.S. Treasury bills. The average annual returns on the portfolio are based on the historical performance of stock and bonds from 1926 through 2022. To increase the illustration’s statistical validity, rolling annual returns are used. Thus, the first retiree lived from 1926 through 1951 and a second retiree lived from 1927 through 1952, and the results reflect the average returns over 73 unique rolling 25-year periods. Each rolling period represents a different retiree’s lifetime and unique results. We’re assuming the starting value of the portfolio is $1 million and reducing the annual portfolio balance by 1% annually to cover annual expenses of mutual funds or exchange traded funds as well as advisory fees. Withdrawing 5% Annually. With this approach, 5% of the portfolio balance is withdrawn at the end of each year. Applying $1 million invested in a 65% stock, 35% portfolio and all the other assumptions listed above, the average total amount withdrawn over the 73 rolling 25-year periods was $2.3 million, and the average portfolio left to heirs at age 90 was $2.65 million. Notably, the 73 retirees withdrew much more than their $1 million starting amount and nonetheless left their spouse and heirs much more than the starting amount. This highlights the power of a percentage-based withdrawal approach. A retirement portfolio is different from tapping water held in a barrel. History shows that portfolios constructed in the prudent manner illustrated here were replenished. Essentially, more water comes into the barrel even as it is being tapped annually for withdrawals. Is this guaranteed? No. But the chances of growing the portfolio while also taking retirement income withdrawals has a history of success. The $92,538 was the average of more than 1,800 annual withdrawals by the 73 retirees. In some years, withdrawals were less than that and some were larger than that, but that's the average. Keep in mind, after a year like 2008 or 2022, when diversified portfolios suffered large losses and both stocks and bonds declined, the withdrawals did decline, providing less income in that year. This is one of the ways a percentage-based withdrawal approach protects the portfolio from being depleted and must be considered as part of a retirement income plan. An advantage of the 5% withdrawal method is that the portfolio survived all 25 years in all 73 rolling periods – a 100% portfolio success rate! That's characteristic of a prudent percentage-based withdrawal approach: It self-corrects. Other withdrawal methods may be more prudent than the 5% method illustrated here depending on your personal situation. For instance, if a retiree’s top priority is withdrawing as much as possible annually while leaving their heirs a significant amount, using other formulas may be better in your situation. If your top priority is leaving more to your spouse and other beneficiaries, a different withdrawal method may be better in your situation. If you’d like to know about better withdrawal options, please contact us. *Large-company stocks represented by S&P 500 Index; small-company stocks by Russell 2000 Index; foreign stocks by MSCI EAFE Index; bonds by Bloomberg Aggregate U.S. Bond Index; Treasury by 3-month Treasury Bills. Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. You should consult the appropriate financial professional regarding your specific circumstances.

The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions.

This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice. |