The Wall Street Journal published an article on October 19 about investing that illustrates the difficulty for investors in understanding the basics of long-term retirement planning. Criticizing America’s No. 1 financial newspaper is not done lightly, and it’s important to see how the press often undermines prudent investing concepts crucial to retirement success. Here goes: One of the best ways to analyze a retirement portfolio’s performance is through rolling time frames. Rolling returns are a useful way to analyze the performance of a retirement portfolio over many different time periods. It offers a more accurate picture than a single period. Rolling returns enable investors to better understand the behavior of a retirement portfolio as actually experienced by retirees. The Wall Street Journal is undermining conservative investors who diversify across asset classes by urging them to abandon their strategy precisely when it’s harder than ever to maintain a long-term strategic discipline and follow the advice of a fiduciary. Only by examining the facts in depth using rolling returns going back 97 years would an investor know that The Journal is undermining investors at the worst time in recent history

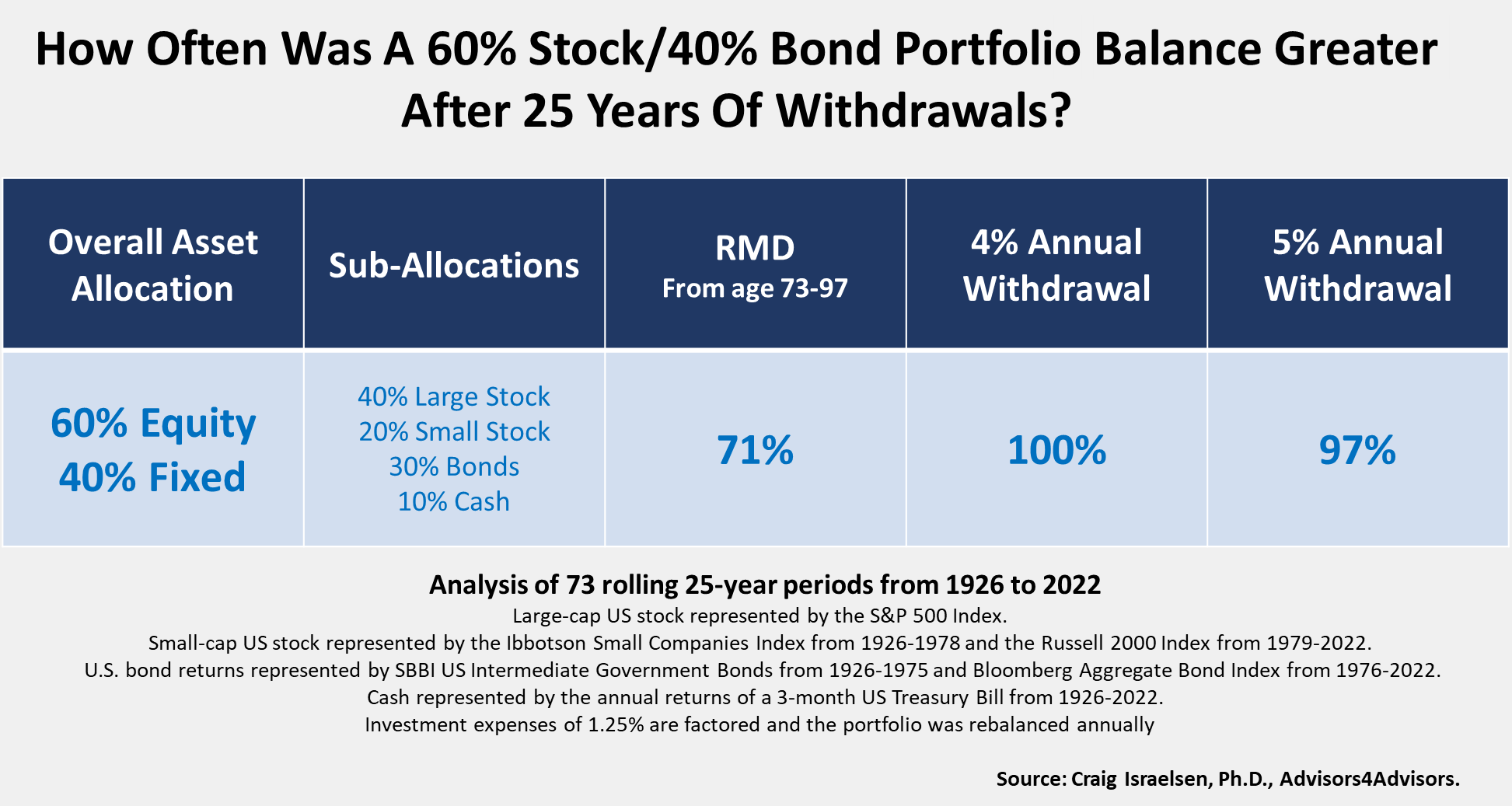

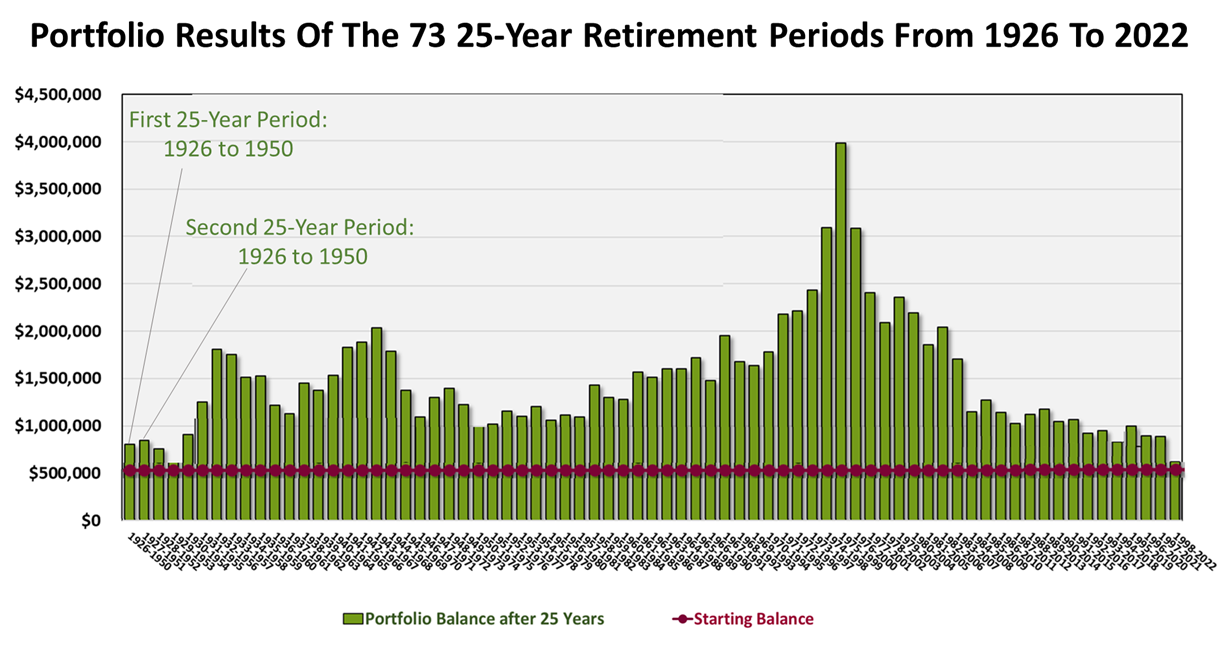

Shown above is a 97-year period, from 1926 through 2022. In these 97 years, there were 73 rolling 25-year periods. We’re assuming 25-year periods to approximate how long a retirement portfolio needs to last. A 25-year period represents the time frame from age 65 to age 90, 66 to 91, and so on. That’s about how long a retiree is likely to need to pull money out of a portfolio annually for income. This chart shows that each of the 73 retirement periods supported a 4% annual withdrawal rate while leaving a retiree’s heirs at least $500,000. The starting balance of each 25-year rolling period was $500,000, 60% invested of which was in stocks and 40% in bonds. After annually withdrawing 4% of the portfolio to live on in retirement, the ending balances of each 25-year retirement period is shown by the green bars. Think of each green bar as a different retiree. In 100% of the 73 retirement journeys – after annual withdrawals of 4% for each of the 25 years – more than the $500,000 a retiree started out with 25 years earlier was left for heirs. A retiree who started with $500,000 in 1975 would have left about $4 million to their heirs after taking 4% withdrawals annually for 25 years. That was the best 25-year outcome. The worst retirement investor experience was the 25 years through 2022, when a little more than $500,000 was left for heirs after 4% annual withdrawals.

Moreover, if a retiree upped annual withdrawals to 5%, the ending balance after 25 years of withdrawals exceeded the starting amount in 97% of the 73 retirement periods examined. But we want to call your attention to the RMD illustration of the required minimum distribution formula. The RMD withdrawal scheme is important because it uses the IRS mandated rules applied to owners of traditional IRAs who are 73 and older. The RMD method adjusts withdrawals annually based on your actuarial life expectancy. It stretches withdrawals as you grow older, which is prudent. To be clear, after you turn 73, the IRS requires you to take withdrawals from a traditional IRA every year using a formula based on your life expectancy, and that formula is used in this illustration because it is mandatory for so many retirees and is also a prudent and practical, widely understood formula based on how long a retiree is likely to live as they grow older. Using the RMD formula, the ending balance of all 73 rolling 25-year periods was more than the starting balance of $500,000 in 71% of the 73 retirement periods studied -- and that is AFTER taking withdrawals every year! To be fair, these numbers are backward looking. They reflect an era very different from what has happened since the pandemic struck in February 2020. For the past year, the yield curve has been inverted; a 90-day Treasury Bill has been priced higher than a 10-year bond, which makes no sense. Holding a 10-year bond for a longer-term historically has guaranteed more income than a short-term T-bill over long-term history. An inverted yield curve is historically a reliable precursor to a recession. The yield of the 10-year/Fed funds rate yield curve has been inverted since January 2023, but no recession is possible with the new-job creation growing its current pace. This is one of numerous post-pandemic anomalies complicating the 2024 investment outlook.

For the last two and a half years, financial economic conditions have been distorted by anomalies stemming from pandemic-related factors, including: - a partial shutdown of the economy after Covid-19 struck in February 2020

- trillions of government stimulus in 2021 and 2022 to prevent economic catastrophe

- Federal Reserve quantitative easing to strengthen the U.S. financial balance sheet

- worst inflation since 1981

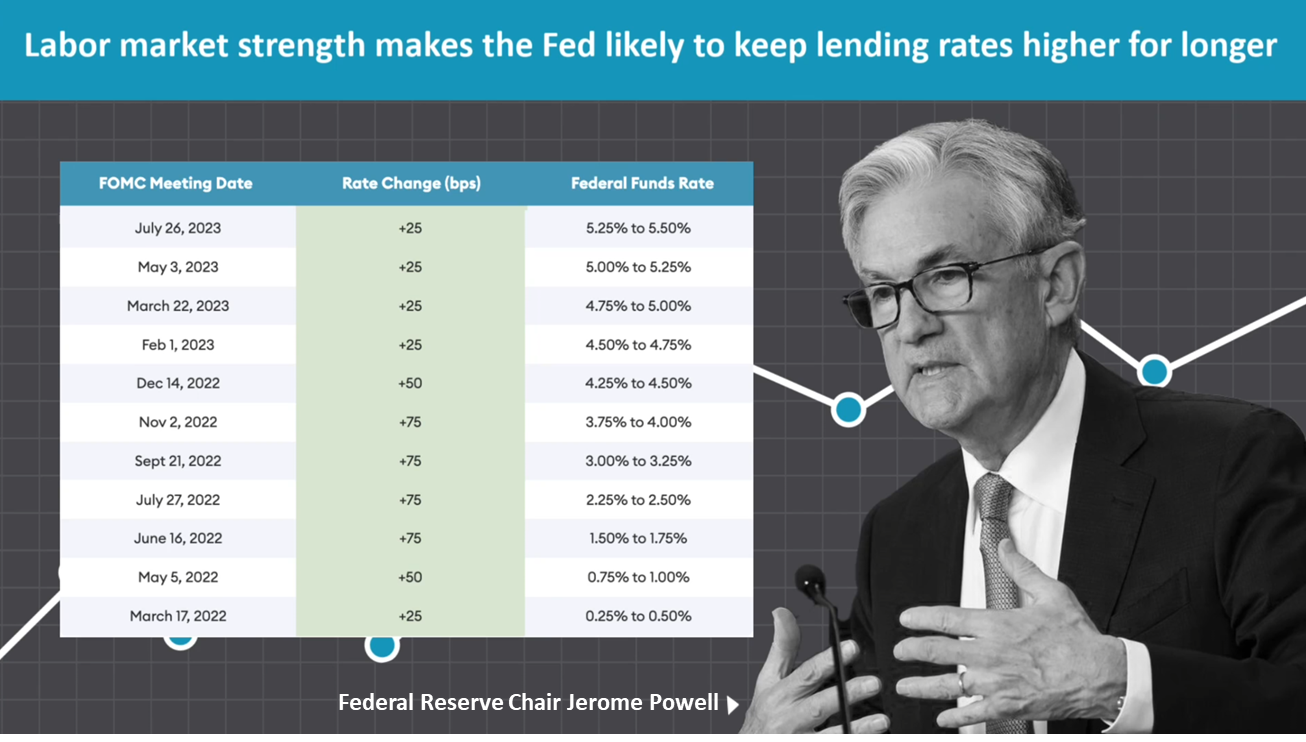

- 11 hikes in U.S. central bank’s lending rate in 19 months (about 1 and a half years) from March 2022 through October 2023

The influence of post-pandemic anomalies faded in recent months, however, and the yield curve is less inverted. It is trending toward normalcy, back to a time much more like the 95 years before the pandemic. Which brings us back to The Wall Street Journal article that pooh-poohed the wisdom of a 60/40 stock and bond portfolio, concluding the classic stock and bond portfolio” isn’t cutting it anymore,” and implying financial advisors are giving bad advice.History shows The Journal treated anomalies of the post-pandemic period as if they will continue in the future. In fact, the recent return to an 8% 30-year mortgage lending rate and 4.8% yield on a 10-year Treasury represent a return to normalcy -- a return to a time when the yield curve makes sense. Our point is The Journal is undermining conservative investors who diversify across asset classes and follow the advice of a fiduciary, to abandon their strategy precisely when retirement investors are likely to find it harder than ever to maintain a long-term strategic discipline. Only by examining the facts in depth using rolling returns going back nearly a century would an investor know that the Journal is undermining investors at the worst time in recent history. If a major financial publication like The Journal can make the mistake of extrapolating recent history into the long run, how is the average American retiree supposed to know the truth of long-term investing? Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. You should consult the appropriate financial professional regarding your specific circumstances.

The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions.

This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice. |