Click image to enlarge

Modern portfolio theory, or MPT, is a framework for investing. It provides the intellectual underpinning of our firm’s approach to investing. Just as constructing the framework for a home is strategically designed by connecting one piece of wood with another, MPT provides a system for constructing a portfolio based on measurable dimensions of investments—history and quantitative characteristics. Owning different kinds of investments is less risky than owning only one type of asset, and MPT is a system for diversifying across a wide range of assets based on their statistical characteristics.

Click image to enlarge

Classifying investments based on their distinct characteristics—such as the aggregate value of a company’s shares outstanding, profit growth, and share-price variance—imposes a quantitative discipline for selecting combinations of investments based on historical data. Investments revolve around a world that is always changing, and not enough statistical history of different kinds of investments exists to make investment predictions about the future with certainty. MPT is a way of managing that uncertainty.

Click image to enlarge

Just as every stud or joist in a home has its own mathematical dimensions, investments have their own unique shapes and characteristics. MPT organizes statistics that measure the characteristics of different kinds of investments to construct a portfolio. MPT is a way of building a portfolio of investments so that the return you can expect over the long run is maximized for a given level of risk. Just as a home can be built to your personal needs and preferences, so, too, can a portfolio be custom-built to suit your personal risk tolerance specifications. To be clear, cookie-cutter portfolios are not what we do. Each portfolio can be tailored to an investor’s preferences.

Click image to enlarge

Economist Harry Markowitz introduced MPT in a 1952 essay. He was awarded a Nobel Memorial Prize in Economic Sciences in 1990. It’s worth noting that it took from 1952 to 1990, 38 years, for Markowitz to be recognized by the Nobel committee. This provides insight into how long it takes for knowledge to be accepted. Over the last 70 years, the power of modern portfolio theory has grown to be understood. It is now the framework for investing embraced by institutional investors worldwide, and it is a foundational element in the curricula of the world’s best colleges and universities. MPT does not guarantee investment success—nothing does—but MPT is embraced by pension funds and other institutional investors, and it is the intellectual underpinning for the performance numbers we’ll share with you in this report.

Click image to enlarge

MPT is a starting point for constructing a quantitatively driven portfolio based on fundamental economics. MPT enables a financial professional with an understanding of the math to adjust what’s happened in the past to devise an investment plan based on economic fundamentals. Just as the laws of physics are relied upon for building a home, fundamental factors of economics are relied upon in constructing a portfolio. For example, we know that 70% of the American economy is accounted for by consumer spending. To measure strength in the economy, monthly data published by the U.S. Government—such as the savings rate, compensation of employees, personal income, and inflation—provide decades of data about trends. The growth of the economy drives investment returns.

Click image to enlarge

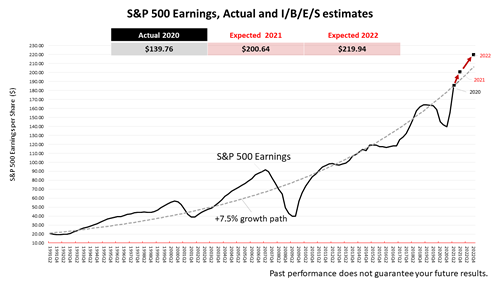

Perhaps the most direct way of connecting the dots between economics and investing is this chart illustrating that what drives stock prices is earnings. Plain and simple, corporate profits—that is, earnings—drive stock prices. The gray dotted line shows the +7.5% long-term earnings growth trend since 1991. In 2020, actual earnings of the S&P 500 companies were $139.76 per share. Expected earnings in 2021, according to Wall Street analysts’ estimates compiled by Institutional Brokers' Estimate System (IBES), are $200.64 per share and are expected to shoot up to $219.94 for 2022. The red arrows drawn in here literally connect the dots to make the forecast clear: The next 20 months’ corporate earnings are expected to rocket much higher.

Click image to enlarge

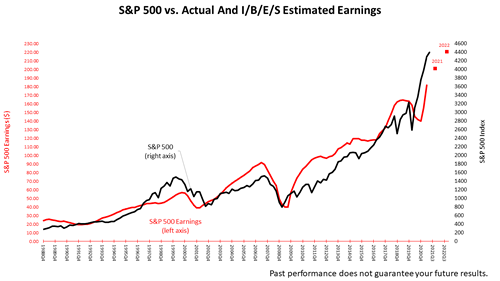

In this chart, to show how earnings drive stock prices, we added the S&P 500 Total Return index, in the black line. This shows the nearly perfect correlation between stock prices and underlying earnings. The 2021 and 2022 earnings forecasts, in the red dots, pull the black line higher.

Click image to enlarge

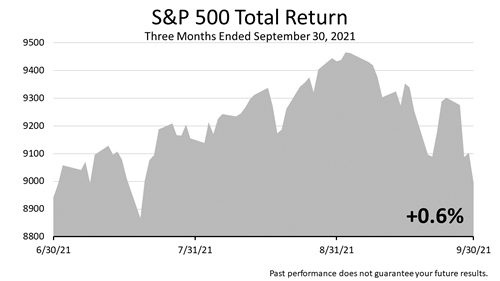

For the quarter, the S&P 500 eked out a gain of six-tenths of 1%. Although the gain was fractional, it was the sixth consecutive quarter in which the S&P 500 showed a positive return since the -19.6% quarterly loss in the first quarter of 2020, when the COVID pandemic struck the U.S. Between the March 23, 2020 bear market low and the end of the third quarter of 2021 on September 30, 2021—18 months plus one week—the S&P 500 total return, including reinvestment of dividends as well as price appreciation, was more than 60%. It’s an astonishing recovery!

Click image to enlarge

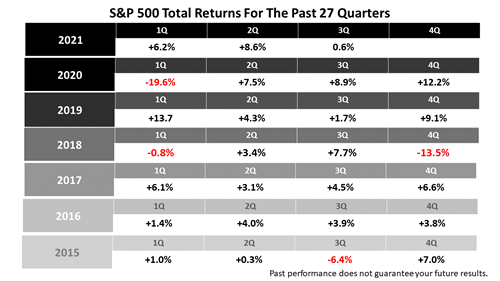

The stock market since 1926 has averaged slightly more than a +10% annual return, averaging a return of about +2.5% per quarter. This table shows the returns in each of the last 27 quarterly periods, one quarter shy of seven years. In the past 27 quarters, the return on stocks was +2.5% or more 18 times. The average quarterly return was less than 2.5% in nine of the past 27 quarters. To be clear, two-thirds of the past 27 calendar quarters showed above-average returns. Keep in mind, this includes a double-digit correction in the fourth quarter of 2018 and the COVID bear market plunge in the first quarter of 2020.

Click image to enlarge

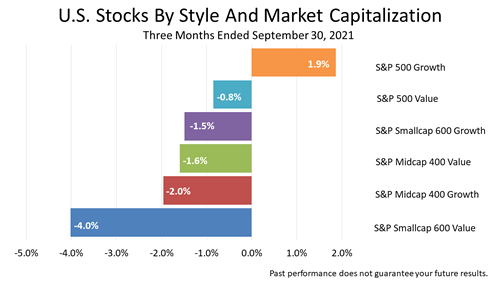

This bar chart highlights how diversification works. By divvying up U.S. companies into these six categories based on their characteristics and statistical history, you can see the difference in returns even over a three-month period. When these differences in returns recur for a few quarters, which can happen from time to time, rebalancing the portfolio to restore it to your preferred risk profile is required.

Click image to enlarge

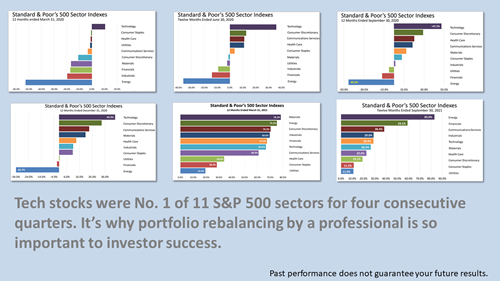

There are many reasons why professional advice may be best for managing your financial situation. Here’s a good one. One of the services our firm offers is portfolio rebalancing. Periodic rebalancing is about as important to investor success as personal advice on tax efficiency. Rebalancing your portfolio is not a sexy-sounding benefit of working with a professional, but it might affect your portfolio’s terminal value about as much as tax-smart investing advice, which is another important reason to hire an investment professional. Automated calculators for rebalancing get the math right, but getting investors to use them to rebalance once a year requires a commitment of time and an interest in personal finance, as well as behavioral change. Working with a qualified professional who knows your financial goals and risk tolerance comes in handy in the period since COVID hit the U.S. Since the pandemic hit in the first quarter of 2020, technology was the No. 1 performer of 11 S&P 500 industry sectors for five consecutive quarters, but for the last two quarters was a middling performer. The 12-month returns for the past six quarters on stocks classified by industry sectors illustrate why a portfolio rebalanced once a year by a professional is so important to investor success. During the pandemic, both the Standard & Poor’s tech sector and the overall index were big winners because shopping online was safer health-wise. So was watching Netflix. And Google ads suddenly were attracting more eyeballs. Apple and Microsoft earnings growth was four times the earnings growth on the average S&P 500 stock, according to Fritz Meyer, an independent economist. It was totally unexpected, of course. The tech sector was the only one of the 11 industry sectors that make up the S&P 500 index to show a gain (10%) in the first quarter of 2020, when COVID hit. It was just the start. For the next three quarters, tech sector 12-month returns for stocks came in at an astonishing +37%, +47%, and +44%. It was an historic bull market kicked off by government transfer payments to consumers, and it is still in progress. But tech stocks for the past two quarters have not been dominating. They’ve now returned to the middle of the pack of the 12-month 11-sector index performance. Successive quarters of outperformance would have allowed your tech stock position to grow unchecked and dominate in your portfolio results. With leadership shifting, a rebalanced portfolio would have been better able to benefit from the change in leadership in the past two quarters. There are many ways to rebalance a portfolio. Rebalancing based on a portfolio’s industry sector weightings is shown for illustration purposes.

Click image to enlarge

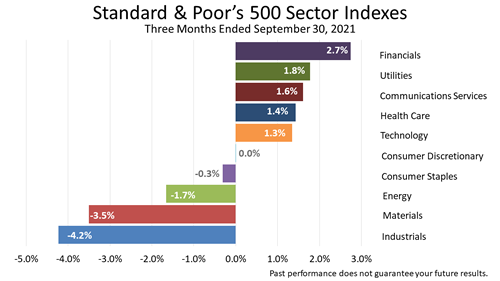

Here is the three-month performance of the S&P 500 stocks through September 30, 2021. Industrials, materials, and consumer stocks took a hit as the Delta variant caused supply chain disruptions. Financials benefited as the yield curve widened, which enabled financial companies to make more money on the spread between long- and short-term interest rates.

Click image to enlarge

While the quarter started off looking quite bright, performance of U.S. companies was hampered throughout the summer by the spread of the Delta variant. Meanwhile, in China, a government crackdown on huge tech companies, like Alibaba Group, caused a drop in China’s fledgling stock market.

Click image to enlarge

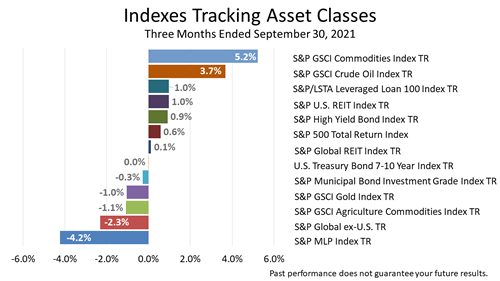

As the world recovered from the pandemic, demand for commodities and oil rose sharply while supply chain disruption sent prices higher. The S&P 500, which has often been atop this three-month chart in recent quarters, fell to the middle of the pack as the Delta variant threatened the strength of the pandemic recovery.

Click image to enlarge

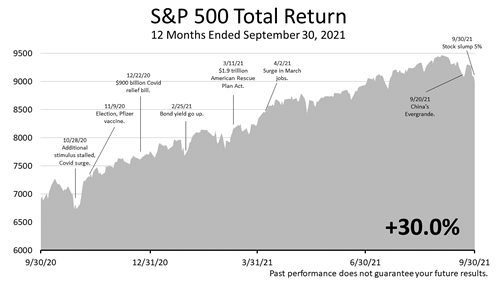

Stocks climbed a wall of worry during the 12 months ended September 30, 2021. The pandemic-plagued economy faced a long list of uncertainties, but the S&P 500 gained 30%. Following massive unprecedented government transfer payments to prop up the economy during the COVID partial shutdown of the economy, Americans were sitting on an unprecedented amount of cash in checking and savings accounts. The consumer economy, which accounts for 70% of U.S. gross domestic product growth, remained extremely strong, but a surge of inflation, supply-chain bottlenecks, and price-to-earnings ratios higher than the historical norm allowed a new round of doubts and fears to spread.

Click image to enlarge

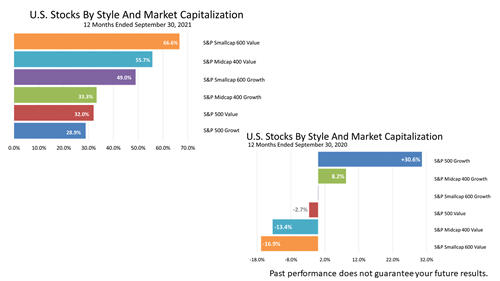

At the upper left is the 12-month total return on U.S. stocks classified by their market capitalization and style. At the lower right is the same 12-month results one year ago. The results one year ago were almost a mirror image for what occurred over the past 12 months. Small-cap value stocks were the top category in the recent 12 months, with a +66.6% return, but this same category was last one year earlier, with a -16.9% loss. The same was true of mid-cap value stocks, which were ranked second-worst among the six categories one-year ago but turned on the second-best return over the most recent 12 months. This is why diversification and rebalancing works.

Click image to enlarge

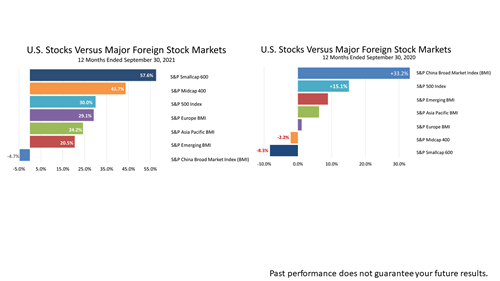

Not to belabor the point, but you can see the same pattern in these two charts comparing returns on seven categories of foreign and domestic stock indexes. In the most recent 12-month period, small-company U.S. stocks returned an astounding +57.6%. But just a year ago, the same chart showed small-caps were the worst performers, with a loss of -8.3% in the preceding 12 months. Similarly, the Chinese stock market index was the No. 1 category, with a +33.2% return, one year ago. But in the more recent 12-month period, on the left, the Chinese stock market lost -4.7% in value. Again, this highlights the wisdom of diversifying and rebalancing.

Click image to enlarge

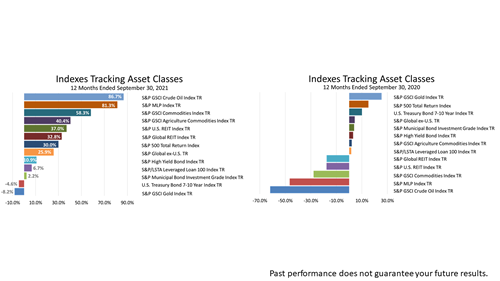

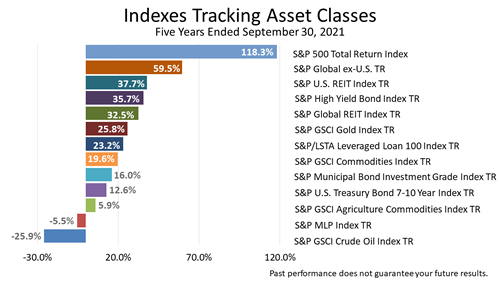

Again, the one-year results of this basket of 13 different asset classes for the period ended September 30, 2021 is almost a mirror image of the same chart one year earlier. Gold was the biggest losing asset in the most recent 12 months, but one year ago it was atop this list. The reversals in the returns of Treasury bonds, master limited partnerships, commodities, and REITs also highlights how unpredictable investing often can be, and underscores the need for a strategic approach based on diversification.

Click image to enlarge

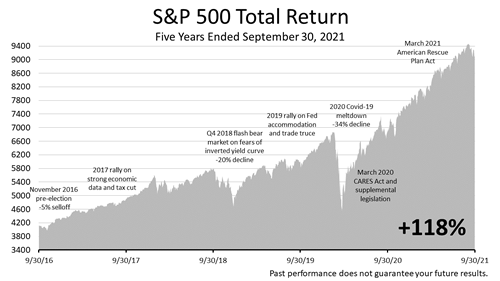

Over the five years ended September 30, 2021, including dividends, the S&P 500 Total Return index gained an astonishing +118%. The five-year gain average annual growth rate was nearly 24%! That’s more than double the stock market’s long-term annual total returns of approximately +10% going back 200 years, as described by Wharton Business School’s professor Jeremy Siegel in his seminal book, Stocks for the Long Run, first published in 1994. Despite the COVID pandemic bear market plunge in February and March 2020, when stocks lost -33.9%, investments in stocks more than doubled in this five-year period which was fraught with uncertainty. The performance of the five largest companies in the S&P 500—Apple, Microsoft, Amazon, Google and Facebook—has led the recovery in stocks since the pandemic low in the Standard & Poor’s on March 23rd, 2020. And, because the major stock indexes are weighted by market capitalization, the super returns on just these tech giants powered the performance of the S&P 500. However, their valuations are not out of control.

Click image to enlarge

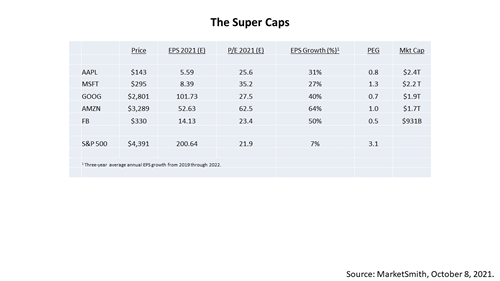

With a $2.4 trillion market capitalization on Apple, and $2.2 trillion market cap on Microsoft, they are expected to grow their profits by +31% and +27%, respectively. As a result, the super caps are trading at low price-earnings-growth—or PEG—ratios relative to the other 495 stocks in the S&P 500 Index. A PEG ratio is a company’s price/earnings ratio divided by its expected earnings growth rate. It adjusts the traditional price/earnings metric for valuing a company’s stock by accounting for its expected earnings growth rate. The five super caps may appear expensive relative to the S&P 500’s average P/E ratio of 21.9, but their earnings growth rate is reflected in the PEG ratios, and they are cheap by this important metric relative to the other 495 companies in the index. For example, the expected earnings growth rate for Amazon is +64%, and its PEG ratio is 1.0%, versus the S&P 500 average PEG ratio of 3.1. Stocks are risky investments and they are volatile. The S&P 500 suffered intraday declines of -2% this past summer, and one-day losses of more than 1%, but it repeatedly bounced back and hit new highs. Uncertainty about the risk of the COVID-19 variant, as well as inflation, is likely to cause big drops in the S&P 500 in the days ahead. Yet stocks are the growth engine of a retirement portfolio and a key in building a tax-smart investment plan with the objective of lasting the rest of your life. This table entitled was derived from a class for financial professionals by Fritz Meyer, an independent financial economist, on Advisors4Advisors on October 13, 2021.

Click image to enlarge

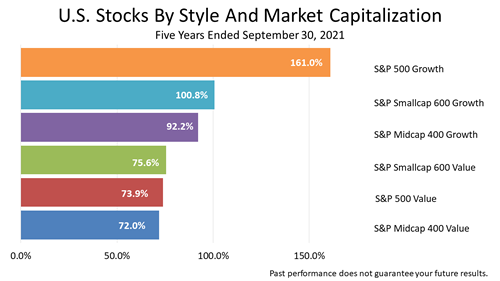

The five super caps were the key factor that drove the five-year return on S&P 500 Growth stock index. Doubling in a five-year period is a marker of an explosive bull market, which makes the large-cap growth stock index’s performance all the more astonishing.

Click image to enlarge

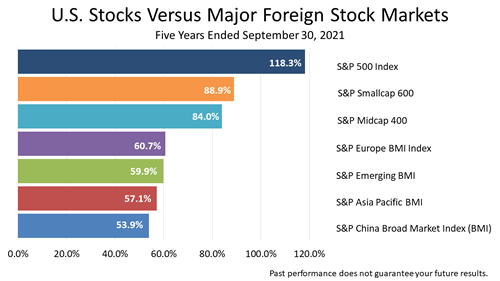

Looking at the major regional stock indexes from different regions across the world shows the dominant performance of the U.S. stock market.

A decade-long bull market was ended by the pandemic-inspired bear market in February 2020, but the U.S., which has led regional bourses for many years, recovered from the COVID outbreak faster, and these stock results are a testament to that resilience.

Click image to enlarge

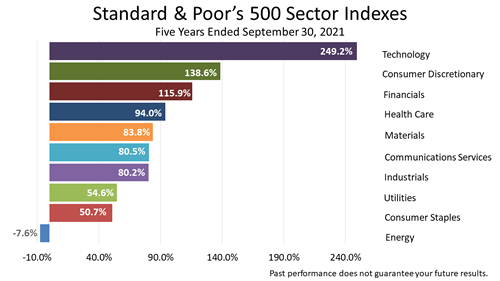

The five super caps drove the astounding return on technology stocks. Though energy stocks led the sector indexes over the 12 months ended September 30, 2021, energy has been a terrible industry sector over the five-year period shown in this chart.

Click image to enlarge

Click image to enlarge

|