Click image to enlarge

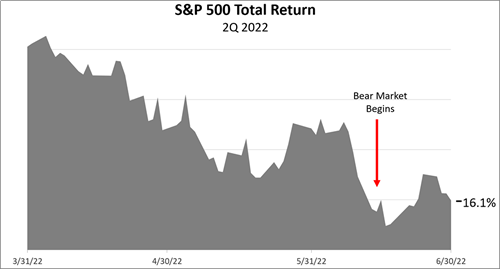

A BEAR MARKET BEGINS The pandemic, Russian war on Ukraine, soaring inflation, rising interest rates, and growing possibility of a recession led a bear market to begin on June 13, when the S&P 500 dropped more than -20% from its January 3, 2022, all-time high. Stocks posted a -16.1% loss in 2Q 2022, after a -4.6% loss in 1Q 2022.

Click image to enlarge

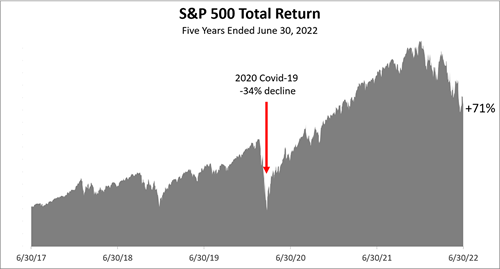

A 12-MONTH WALL OF WORRY Despite the back to back quarterly losses, the S&P 500 stock index over the five years ended June 30, 2022, showed a total return, including dividends, of +71%. The five year period included the pandemic market meltdown of February and March 2020, when the stock market lost -34% of its value.

Click image to enlarge

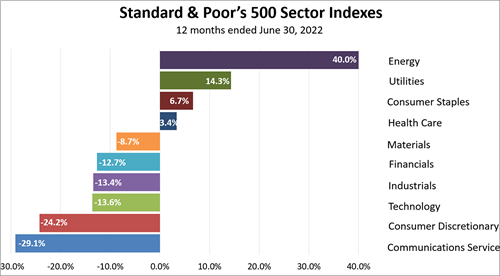

INDUSTRY SECTORS Higher energy prices propelled energy companies to the top of the 10 industry sectors in the S&P 500 stock index, with a +40% return in the 12 months ended June 30. Energy was No. 1 for the past four quarters but it was the worst performer for the five previous quarters starting in 4Q 2019.

Click image to enlarge

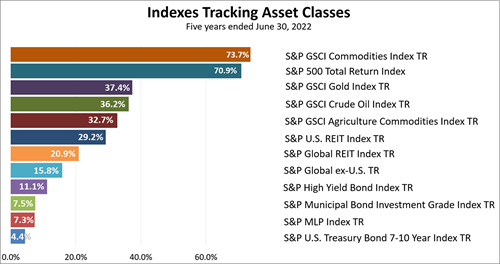

INDEXES TRACKING 13 ASSET CLASSES Despite being in the throes of a bear market, No. 2 of the broad array of 13 investments for the five years ended June 30 was U.S. stocks. The other top performers were commodity, gold, and energy investments, all of which are more volatile than the S&P 500 index. Bonds and non-U.S. equities lagged by a wide margin.

Click image to enlarge

CONSUMERS ARE IN THE BEST SHAPE EVER Household net worth surged like never before during the pandemic. Entering this downturn, household balance sheets were exceptionally strong. With consumers accounting for 70% of U.S. economic activity, this unusual support for continued consumer spending, suggests a short, shallow downturn.

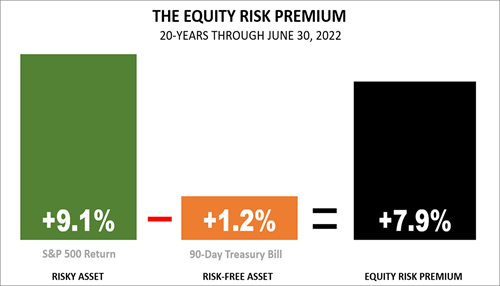

Click image to enlarge

NO SUCH THING AS A FREE LUNCH Amid a bear market, remember this is what you signed signed-up for: a risky asset subject to periodic bear market drops of 40% or even 50%. This is why equities paid a premium over risk-free U.S. Treasury Bills for the past 20 years, which included bear markets in 2002, 2008, and early 2020. Past performance is never a guarantee of your future results. Indices and ETFs representing asset classes are unmanaged and not recommendations. Foreign investing involves currency and political risk and political instability. Bonds offer a fixed rate of return while stocks fluctuate. Investing in emerging markets involves greater risk than investing in more liquid markets with a longer history. Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk of loss. Sources: Sector performance data from Standard and Poor’s. Household net worth data through March 2022 from Federal Reserve Bank of St. Louis, released June 9, 2022; Equity risk premium data from Craig Israelsen, Ph.D, Advisors4Advisors.

|